03-16-2026

What Is the $2,500 Expense Rule and How It Affects Truckers & Fleet Owners?

{kind=link}

{kind=link}

Truckers and fleet owners make dozens of “small” purchases that keep equipment rolling, tires, parts, safety gear, tablets, shop tools, and sensors. The tax challenge is that the IRS does not treat every purchase the same way. Some costs are deductible right away, others must be capitalized and recovered over time.

One of the most practical tools for simplifying this is the $2,500 expense rule, often discussed as a way to reduce paperwork and improve cash flow.

What is the $2500 expense rule?

What is the $2500 expense rule? It is the common name for the IRS de minimis safe harbor election under the Tangible Property Regulations. In plain English, it lets many businesses deduct (expense) qualifying items that cost $2,500 or less per invoice or per item, instead of capitalizing them.

For trucking businesses, this can matter because you often buy lots of mid-priced items that are business necessities but not “big equipment” purchases.

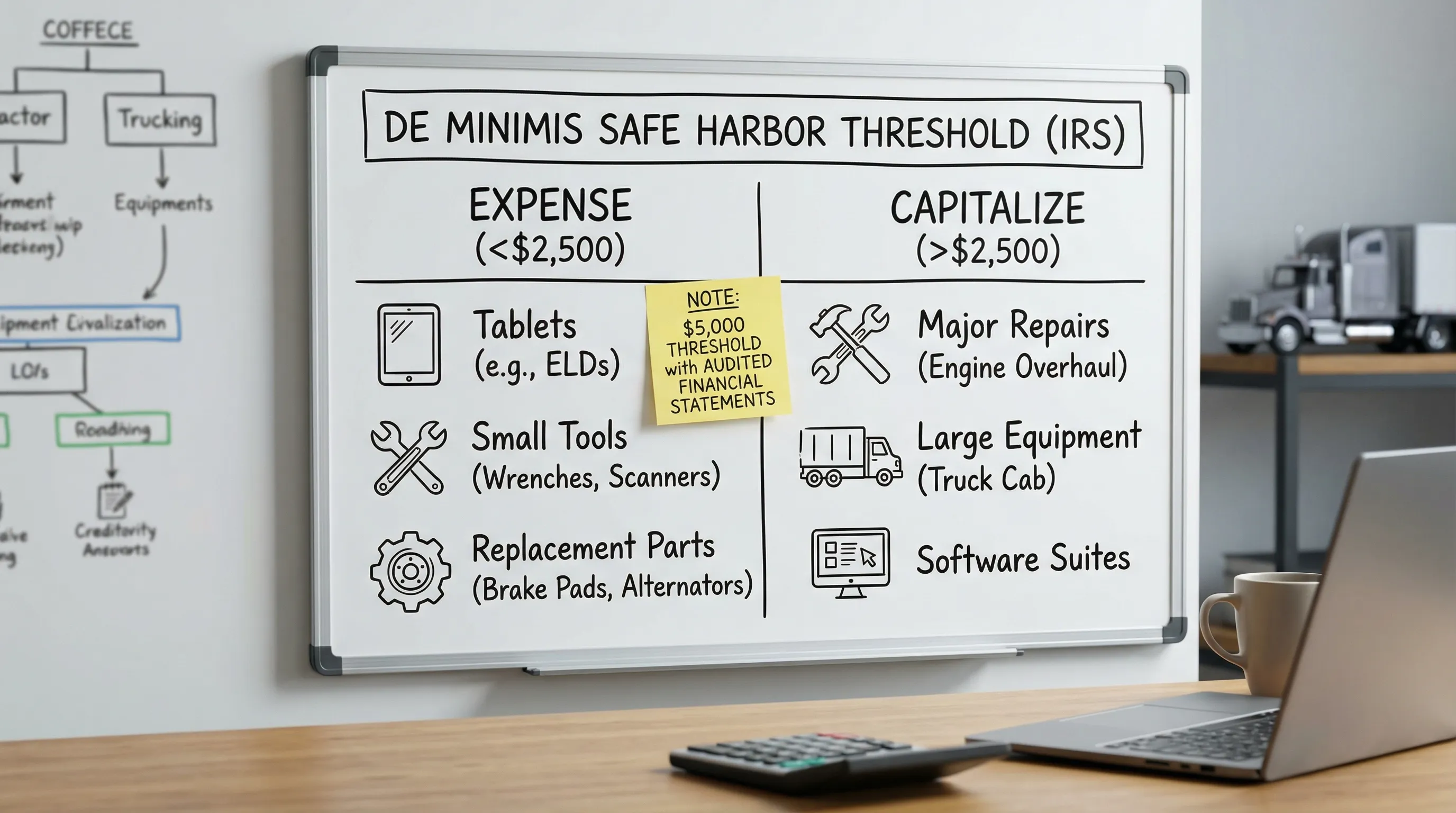

The two thresholds: $2,500 vs. $5,000

The threshold depends on whether you have an Applicable Financial Statement (AFS), typically an audited financial statement.

| Business type (simplified) | De minimis safe harbor threshold | What it means for most fleets |

|---|---|---|

| No AFS (common for owner-operators and many small fleets) | $2,500 | Many everyday purchases can be expensed if you follow the rules |

| Has AFS (audited statements) | $5,000 | Higher threshold, more purchases qualify |

The IRS increased the non-AFS threshold to $2,500 through IRS Notice 2015-82, which is why you see this amount referenced so often.

Why truckers and fleet owners feel this rule more than most industries

Trucking has a steady stream of operational purchases that often land in the $200 to $2,500 range:

- ELD or dispatch tablets and mounts

- Replacement sensors, cameras, and in-cab electronics

- Small shop equipment (jacks, torque wrenches, battery chargers)

- Safety equipment and securement gear

- Trailer parts, lights, mud flaps, hoses, and similar items

The difference between expensing and capitalizing is not only “tax theory.” It affects:

- How quickly you get the deduction (this year vs. over several years)

- How clean your bookkeeping is at year-end

- How confidently you can forecast estimated taxes and cash needs

A cost reality check (data point for planning)

Industry benchmarking consistently shows that maintenance and repairs are among the major operating cost categories. ATRI’s annual operational cost research is widely used for budgeting, and you can review the latest report here: ATRI Operational Costs of Trucking.

Even if your numbers differ from national averages, the takeaway is consistent: maintenance-related spending is frequent, and anything that reduces friction in tracking and categorizing those purchases is strategically valuable.

How the rule works in practice (the 4 requirements you cannot ignore)

To use the $2,500 expense rule correctly, focus on the mechanics:

1) It applies per invoice or per item

If an invoice lists multiple items, you generally look at the per-item cost. If the invoice is lumped into one line, the IRS may treat it as one item.

This creates a real-world fleet lesson: itemized invoices are tax assets.

2) You need an expensing policy in place at the start of the year

- If you have an AFS, the policy must be written.

- If you do not have an AFS, IRS rules refer to “accounting procedures,” and most tax pros still recommend documenting them in writing for audit defense.

3) You must expense it on your books

If you capitalize it in your accounting records, you generally cannot claim the safe harbor deduction for it on the return.

4) You must make the election every year

This is not automatic forever. The safe harbor is elected annually by attaching a statement to the timely filed tax return.

For the formal framework, see the IRS overview of the Tangible Property Regulations and related guidance: IRS Tangible property final regulations.

The trucking-specific gray area: repairs vs. improvements (and why the safe harbor is not a magic wand)

A common misconception is: “If it’s under $2,500, I can always expense it.” Not always.

Two concepts overlap:

- Repair vs. improvement rules (whether something must be capitalized because it betters, adapts, or restores a unit of property)

- De minimis safe harbor (a separate election that can allow expensing smaller amounts if requirements are met)

In practice, most “big” truck events that clearly restore or rebuild equipment (engine overhaul, major rebuilds) tend to exceed $2,500 anyway. But fleets run into edge cases, especially when vendors bundle work.

Strategic lesson: how your invoice is written can change the tax treatment. If a shop invoice is vague, your accountant may have to default into conservative capitalization.

Actionable examples for truckers and fleets (illustrative scenarios)

These examples are representative of situations fleets see frequently. They are for planning, not tax advice.

Example A: The itemization advantage (same spend, different outcome)

A fleet buys multiple components during a mid-year refresh.

- Scenario 1 (itemized invoice): 6 tablets at $650 each + mounts at $85 each.

- Scenario 2 (lumped invoice): “Technology package for trucks: $4,410.”

Under the de minimis safe harbor logic:

| Invoice style | What the IRS may view as the “item” | Likely result |

|---|---|---|

| Itemized | Each tablet ($650) and mount ($85) | More likely to qualify under $2,500 threshold |

| Lumped | One package ($4,410) | More likely to be treated as over threshold and capitalized |

Fleet playbook: ask vendors to itemize invoices (especially for electronics, shop tools, and multi-part installs).

Example B: Shop equipment over $2,500 (use other tools)

A small carrier buys a diagnostic tool for $3,200.

This likely does not fit the $2,500 safe harbor threshold. In that case, the decision often becomes:

- Capitalize and depreciate normally, or

- Consider other depreciation options such as Section 179 (eligibility depends on your facts), and monitor bonus depreciation rules. IRS Publication 946 is the starting point for depreciation planning: IRS Pub. 946.

Strategy trend (2026 planning): Because bonus depreciation has been scheduled to phase down over time under prior law, many businesses have paid closer attention to timing of “placed in service” dates and documentation. Talk with your tax pro before making big timing moves.

Example C: Fleet discipline that investors and lenders actually like

Even if you are not seeking outside investment, “investor-grade” recordkeeping helps with financing and audits.

A fleet that can produce clean documentation quickly (purchase date, amount, purpose, asset vs. expense logic) often looks less risky to:

- Equipment lenders

- Insurance auditors

- Potential buyers of the business

The $2,500 rule supports that discipline because it pushes you toward repeatable purchasing and documentation standards, rather than one-off judgments.

What to track so the rule helps, instead of creating a mess

Truckers often call these “IRS tax papers,” but what you want is a system that connects purchases to vehicles and compliance.

Keep these items consistent across your fleet:

- Itemized invoices and receipts (especially when multiple parts are on one ticket)

- A clear link to the unit (truck/trailer number) and, when relevant, the vehicle identification number (VIN)

- Notes that explain “why” when it is not obvious (safety compliance, replacement, minor upgrade)

- A copy of your expensing policy (and ensure your bookkeeper applies it consistently)

How this connects to HVUT filing, IRP truck registration, and Schedule 1

The $2,500 rule is an income tax concept, while Form 2290 is an excise tax filing (HVUT). They are different, but the operational workflow overlaps in one big way: documentation.

When you renew plates or handle Form 2290 and IRP registration, you typically need your Form 2290 Schedule 1 (stamped proof of payment) for the vehicles you are registering.

That is why many fleets standardize two parallel habits:

- Clean, itemized purchase records for tax and cost control.

- Fast, retrievable compliance records for HVUT and IRP.

If you want to reduce compliance friction, using an IRS Authorized E-file Provider can help you electronic file Form 2290 and pay online, then quickly retrieve your Schedule 1 when a state asks for it.

Simple Form 2290 is an IRS-authorized platform built for that workflow, including Easy 2290 filing and document retrieval for owner-operators and fleets. It is also designed for bulk and fleet filing, which matters when you are managing dozens (or hundreds) of VINs and need Schedule 1 copies on demand.

For deeper HVUT and IRP context, see Simple Form 2290’s guide on IRP registration and its breakdown of Schedule 1.

The practical checklist: make the rule work for you this year

Most problems with the $2,500 expense rule come from inconsistency, not from the rule itself.

- Align with your tax pro on a $2,500 expensing policy before year-end.

- Train whoever pays bills to request itemized invoices.

- Reconcile bookkeeping categories so “expensed on books” matches what you intend for taxes.

- Store key compliance documents (including your 2290 Schedule 1 for IRP) in one place so renewals do not turn into a scramble.

If you treat the rule as part of a larger operating system, not just a deduction trick, you will usually see the biggest benefit: fewer surprises, cleaner records, and faster decisions when it is time to scale or finance equipment.

This article is for general informational purposes and is not tax advice. Consult a qualified tax professional about your specific situation.