03-30-2026

PTIN Login for Tax Preparers: When It’s Required for Filing Simple Form 2290

{kind=link}

{kind=link}

If you prepare Heavy Vehicle Use Tax (HVUT) returns for clients, “PTIN login” can feel like an unnecessary extra step. In reality, it is a compliance signal: it helps identify when a paid preparer (not the trucking business owner) is preparing and submitting Form 2290.

This matters because Form 2290 is often filed under time pressure to secure a stamped Form 2290 Schedule 1, which many states and IRP jurisdictions require for IRP truck registration and plate renewal. The cleaner your preparer workflow is, the fewer last-minute rejected returns, VIN problems, and registration delays your clients face.

What “PTIN login” means (and what it does not)

A Preparer Tax Identification Number (PTIN) is the IRS-issued identifier used by paid tax return preparers. The IRS generally requires a PTIN for anyone who prepares, or assists in preparing, federal tax returns for compensation. (See IRS guidance on PTIN requirements.)

For Form 2290 work, a PTIN is most relevant when:

- You are filing as a paid preparer for multiple trucking clients.

- Your name and PTIN belong in the “Paid Preparer Use Only” section of the return.

A PTIN is not the same as:

- An EIN (Employer Identification Number), which is the taxpayer’s business ID used to file Form 2290.

- An IRS e-services login.

- A payment credential (you can still electronic file Form 2290 and pay online without a PTIN if you are the business filing its own return).

When PTIN login is required for filing Simple Form 2290

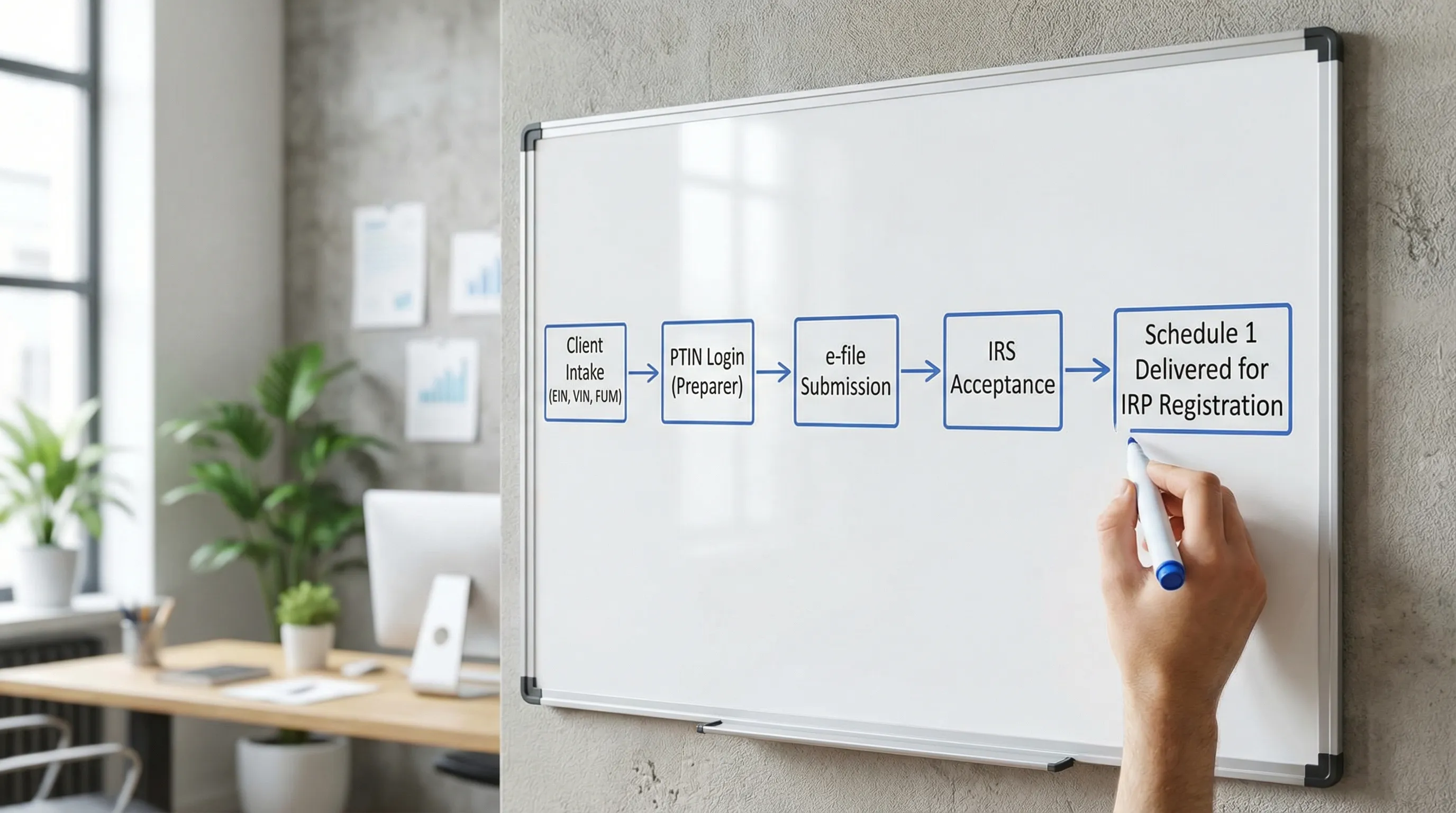

Here is the practical rule of thumb: PTIN login is required when you are acting as a paid preparer filing Form 2290 for someone else, and the software workflow needs to capture your preparer identity.

If the trucking business (owner-operator, dispatcher, office manager) files its own return, PTIN login is typically not required.

Decision table: PTIN login required or not?

| Scenario | Who is filing? | PTIN login usually required? | Why it matters |

|---|---|---|---|

| Owner-operator files their own HVUT | Taxpayer | No | The filer is the taxpayer, not a paid preparer |

| Fleet admin files for their employer (W-2 employee) | Taxpayer’s employee | No | Internal filing generally is not “paid preparer” activity |

| CPA, CTEC preparer, or paid service bureau files for clients | Paid preparer | Yes | Preparer identity (PTIN) must be associated with the prepared return |

| Trucking company outsources HVUT to a third party during peak season | Paid preparer | Yes | Helps document who prepared the return if issues arise |

| You only provide data entry help but do not prepare “substantially all” | Depends | Maybe | PTIN requirement depends on the level of preparation activity (follow IRS PTIN rules) |

Important: requirements can vary by facts and circumstances. If you are unsure whether your role triggers PTIN requirements, verify with IRS guidance and your professional standards.

Why this is trending: compliance speed is now a registration bottleneck

Form 2290 is not just a “tax form for tax return” compliance. It is operational infrastructure for trucking.

Two forces have made PTIN-ready workflows more important for preparers:

- IRP and DMV timing pressure: Fleets often need the stamped 2290 Schedule 1 for IRP quickly. Delays can sideline equipment.

- Peak-season volume: Many preparers handle HVUT filings in bursts, clustered around annual deadlines and fleet renewal periods.

The underlying math is simple. If a client files by paper, IRS processing can take weeks. If they e-file through an IRS Authorized E-file Provider, acceptance and the stamped Schedule 1 are typically much faster.

Turnaround comparison chart

| Filing method | Schedule 1 availability (typical) | Best for | Primary risk |

|---|---|---|---|

| IRS e-file via authorized provider | Minutes to hours after IRS acceptance | IRP deadlines, last-minute filings | Data errors (VIN/EIN/FUM) can still cause rejection |

| Paper filing by mail | Often 4 to 6 weeks (or longer in peak season) | Edge cases, no internet workflows | Late registration, lost mail, slow corrections |

The takeaway for preparers: PTIN login is a small step that supports a much larger outcome, faster client compliance and fewer registration interruptions.

PTIN login vs EIN: the most common preparer mistake

A high percentage of Form 2290 rejections and delays come from identity mismatches, not tax calculations.

- EIN identifies the trucking business that owes HVUT.

- PTIN identifies you (the paid preparer) if you are preparing the return for compensation.

A simple internal control that works well in practice is to store client “identity data” separately from vehicle data:

- Client legal name and EIN (must match IRS records)

- Mailing address (often differs from IRP/garage address)

- Signer authority and contact

- Preparer identity (PTIN) when applicable

This reduces the rework loop where a correct vehicle list still results in a rejected submission.

How tax preparers can file “Easy 2290” returns efficiently in Simple Form 2290

If your goal is an Easy 2290 workflow you can repeat across dozens of clients, standardize the intake first, then file.

Most preparers can shorten cycle time by collecting the same “minimum viable dataset” every time:

- EIN and legal business name

- First Used Month (FUM)

- Vehicle Identification Number (VIN) for each unit

- Taxable gross weight category (and logging/agricultural status if relevant)

- Payment method selection (EFTPS, direct debit, check, etc., per IRS options)

For fleets, the operational advantage is using Bulk and fleet filing capabilities so you are not keying VINs one by one. Simple Form 2290 is built to support fleet workflows, including bulk entries, guided steps, and retrieval of filed returns.

If you need to refresh process details, reference official IRS documents like the Form 2290 page.

Strategic advice: treat Schedule 1 as a deliverable, not an output

For clients, the real deliverable is usually not “the return.” It is Schedule 1.

That changes how a preparer should manage work:

- Build your checklist around “Schedule 1 in hand,” not “submitted to IRS.”

- Track accepted, rejected, and resubmitted filings during peak weeks.

- Maintain a secure archive, so clients can retrieve Schedule 1 later for renewals or audits.

Simple Form 2290 supports fast delivery of the IRS-stamped Schedule 1 after acceptance, which is exactly what many fleets need to keep IRP and registration workflows moving.

To align expectations with reality, point clients to deadlines and explain that the schedule 1 form 2290 due date depends on the first-used month rules (and annual deadlines). For current dates, use a single source of truth such as Simple Form 2290’s Form 2290 due dates guide.

Lessons learned from real-world filing patterns (and how to avoid them)

Across preparer practices, a few patterns show up every year:

The “VIN scramble” problem

A client sends a vehicle list from a registration system, a maintenance sheet, or a dispatch tool. One character is off, and the return gets rejected.

Practical fix: validate VINs at intake. Even a basic “double-entry check” for high-volume clients reduces rejections dramatically.

IRP registration gets blocked by a missing or outdated Schedule 1

Many clients learn late that Form 2290 and IRP registration are connected. If their IRP renewal is due, they need the stamped Schedule 1.

Practical fix: set an IRP-aware calendar and aim to file early, not on the last day.

Weight changes trigger amendments that get overlooked

When a vehicle’s taxable gross weight increases into a higher category, the client may need an amendment (often referred to as Taxable Weight Amendments).

Practical fix: ask one question during quarterly check-ins, “Any units re-rated heavier since the last filing?” If yes, route them to the amendment workflow. Simple Form 2290 provides guidance and filing support for taxable weight amendments.

A quick comparison: in-house filing vs paid preparer filing

PTIN login is not just a compliance checkbox, it reflects a business decision.

| Option | Best fit | Pros | Cons |

|---|---|---|---|

| Client files themselves | Owner-operators, simple accounts | Lower cost, direct control | Higher risk of missed details (VIN, FUM, weight), less support |

| Paid preparer files (PTIN login) | Fleets, multi-entity owners, time-constrained operators | Standardized process, fewer surprises during IRP time, support during rejections | Service cost, intake coordination required |

If your firm serves fleets, the paid preparer model tends to be “cheaper” in the operational sense, fewer late penalties, fewer truck-down days, fewer last-minute IRP problems, even if the filing fee itself is not the absolute cheapest 2290 e file on the market.

Putting it together

Use this simple framing:

- If you are the taxpayer filing your own return, you typically do not need PTIN login.

- If you are a paid tax preparer filing Form 2290 for clients, PTIN login is typically required because your preparer identity must be recorded.

When you combine PTIN-ready workflows with an IRS Authorized E-file Provider like Simple Form 2290, you can build a repeatable “Simple 2290” process: clean intake, fewer rejections, faster accepted returns, and Schedule 1 delivery that supports IRP registration timelines.

For a refresher on return tracking and acceptance statuses, see Simple Form 2290’s guide on how to check 2290 filing status.